Are Gilt Funds the most secure bet after the Franklin episode?

Gilt funds invest primarily in Government securities (G-secs) issued by the RBI on behalf of the Government. Since it invests in bonds that are of highest credit quality, capital protection is more or less guaranteed.

With redemption pressures mounting from its investors, Franklin Templeton mutual fund recently announced the closure of its six credit risk funds. Some of them invested in risky corporate bonds that were becoming difficult to sell in this tight liquidity situation.

Under these circumstances, some investors are now contemplating shifting their debt allocation towards gilt funds. Does it make sense for investors?

Let’s, first of all, understand gilt funds.

Gilt funds invest primarily in Government securities (G-secs) issued by the RBI on behalf of the Government. Since it invests in bonds that are of the highest credit quality, capital protection is more or less guaranteed. Unlike corporate bonds, G-secs have a negligible risk of default (or credit risk).

However, gilt funds carry other types of risk that you need to be aware of.

Types of risk

All type of debt funds carry three types of risk – credit risk, liquidity risk and interest rate risk. While credit risk as mentioned is essentially about the risk of default in repayments by the borrower, liquidity risk is about the inability to easily sell securities in the market. Usually, low rated-bonds (AA or below) have higher liquidity risk than that of benchmark G-secs.

Last but not least is the interest rate risk which is the susceptibility of the bond prices to the changes in the interest rates in the economy. Under an increasing interest rate regime, the returns from gilt funds fall, thanks to the inverse relationship between bond prices and interest rates.

Higher the maturity of the government bonds, more volatile their prices. For instance, the price of a five-year government bond falls by five per cent for every one per cent increase in interest rates and vice-versa. With most gilt funds holding bonds with maturity ranging from five to 10 years, they are highly susceptible to interest rate movements in the economy.

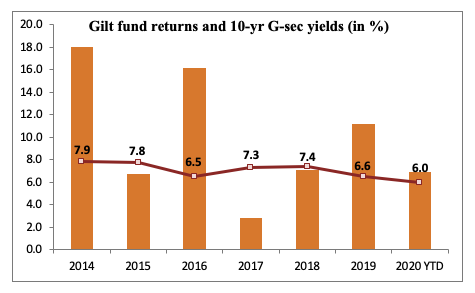

Interest rate movements are not unidirectional. It is currently hovering at multi-year lows with higher odds of interest rates going up. With average maturity of G-sec holdings at 8.8 years for gilt funds, there are chances of gilt funds posting negative returns if interest rates rise consistently. Remember, in the calendar year 2017, gilt funds posted a minuscule return of 2.8 per cent, when interest rate rose by about 80 basis points.

Don’t go by past returns

Bond yields of 10-year government bonds – a barometer of the interest rate in the economy – were down from 7.03 per cent a year back to little less than six per cent now. This, in turn, has resulted in a big appreciation of long-term bond prices. Gilt funds, on an average, have given a return of 15.7 per cent in the last one year, which is next only to that of Gold funds.

The track record of gilt funds looks impressive – in the last three, five and 10 years, it gave a CAGR of 8.6 per cent, 9.0 per cent and 8.7 per cent respectively.

Does that make a strong case for investing in gilt funds? Not really.

Interest rate movements are not unidirectional. It is currently hovering at multi-year lows with higher odds of interest rates going up. With average maturity of G-sec holdings at 8.8 years for gilt funds, there are chances of gilt funds posting negative returns if interest rates rise consistently. Remember, in the calendar year 2017, gilt funds posted a minuscule return of 2.8 per cent, when interest rate rose by about 80 basis points.

Investors, therefore, need to proceed with caution without getting lured by past returns. Moreover, there is weak demand for government bonds in the market now. Foreign Portfolio Investors (FPI) on the one hand are selling heavily, while local banks are wary of investing, fearing a rise in yields (and reporting of losses).

Goal orientation

Moreover, choice-making of instruments has to be in sync with the financial goal in mind. Once you arrive at an asset allocation for it, you need to choose from various debt funds in the offing.

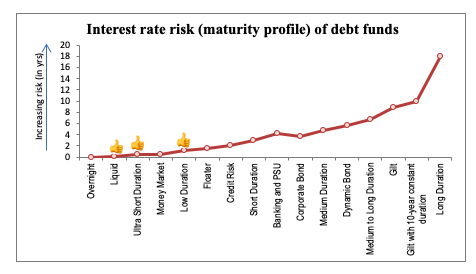

As you can see from the above chart, interest rate risk is highest for long duration and gilt funds. For liquid, ultra-short duration and low duration funds, the risks are far lower. For your debt requirements, a combination of investments in these three low-risk debt fund categories should suffice. It will outperform the returns of Bank fixed deposits and protect capital. To beat inflation, however, your portfolio needs the support of equities.

Takeaway

Gilt funds carry negligible risk of default from the borrower, but takes huge interest rate risk. With interest rates seemingly bottoming out, any increase could correct bond and NAV prices sharply. Stick to liquid, ultra-short duration and low duration funds for your debt portfolio allocations.